Most people do not struggle because they earn less. They struggle because they cannot clearly separate needs vs wants. I have seen this closely in my own spending habits.

There was a time when I thought I was handling my money well. I paid my bills on time. Saved some. I didn’t do anything. At the end of each month, I always wondered was I really doing okay?

I had no idea where my money was going. I was earning decently. My expenses were normal. I thought I was doing right. Somehow, at the end of the month, my money seemed to have disappeared. Managing money is not that easy.

“Where did my money actually go?” That was the first sign that something was off.

What Are Needs and Wants?

Let us keep this simple and practical.

1. Needs

Things we need are the expenses that we have to pay so that we can live and function. We all have these needs. They are very important for our daily life. Needs are the expenses that we must pay every month to live a normal life.

For examples:

- Rent or basic housing

- Food and groceries

- Electricity and water

- Basic transportation

- Essential healthcare

If you remove these, your daily life gets disrupted.

2. Wants

Wants are things that improve your lifestyle, but are not necessary.

Examples:

- Ordering food frequently

- Expensive gadgets

- Branded clothes

- Subscriptions you rarely use

You can live without them. But you choose not to.

This is the real difference between needs and wants:

- Needs to support survival.

- I want to support comfort.

Comparison Table:

| Feature | Needs (Essential) | Wants (Lifestyle) |

| Meaning | Things you must have to live. | Things you wish to have for fun. |

| Priority | High (Must pay first). | Low (Can wait). |

| Effect | Life is hard without them. | Life is normal without them. |

| Examples | Food, Rent, Medicine, Bills. | Dining out, New iPhone, Movies. |

Where I Personally Got It Wrong

I think the biggest mistake I made was not spending much money. It was actually putting the labels on things. I used to think that things that made me feel good were things I really needed.

For example:

- Ordering food after a long day felt like a “need”.

- Upgrading my phone felt “important”.

- Buying better clothes felt “necessary for confidence”.

Individually, none of these felt wrong. But together, they were silently eating my savings. That is when I realized something simple: Most financial problems do not come from big expenses. They come from repeated small wants.

Needs vs Wants Examples (Real-Life Situations)

Let us break down needs vs wants examples you actually face:

Situation 1: Food

- Cooking at home → Need

- Ordering from a restaurant → Want

I used to get food delivered to my place three to four times a week. The reason was not that I really needed it. Food was just easy to get. I mean, who does not like food when it is easy to order. I was getting food because it was simple.

Situation 2: Phone

- A basic smartphone → Need

- Latest high-end upgrade → Want

I upgraded my phone once without any real reason. The old one was working fine.

Situation 3: Travel

- Daily commute to work → Need

- Weekend luxury trip → Want

I think traveling is okay. The thing that bothers me is when people say they need to travel. Traveling is something people can do if they want to. Saying they need to travel is not really true. Traveling is fun. People can live without it.

Situation 4: Clothing

- Basic office wear → Need

- Trend-based shopping every month → Want

I realized that I was purchasing clothes for no reason, just because they were on sale. The thing is, clothes can be something we need or something we just want.. That is where things get mixed up. I mean, the category of clothes can include things that are essential and things that are not, and that is where the confusion happens with clothes.

How to Identify Needs and Wants?

Once I identified my spending problem, I started using a simple mental filter. This approach changed how I look at every purchase.

I asked myself 4 questions before spending:

- Will my life get affected without this?

- Is this something I regularly need to function?

- Am I buying this for survival or satisfaction?

- Can I wait 48 hours before buying this?

I used to make mistakes at the beginning. Over time, things got better. I understood things more clearly. The easiest way to figure out what I need and what I want is to keep things simple and not think about it too much. This way of identifying my needs and wants really works for me.

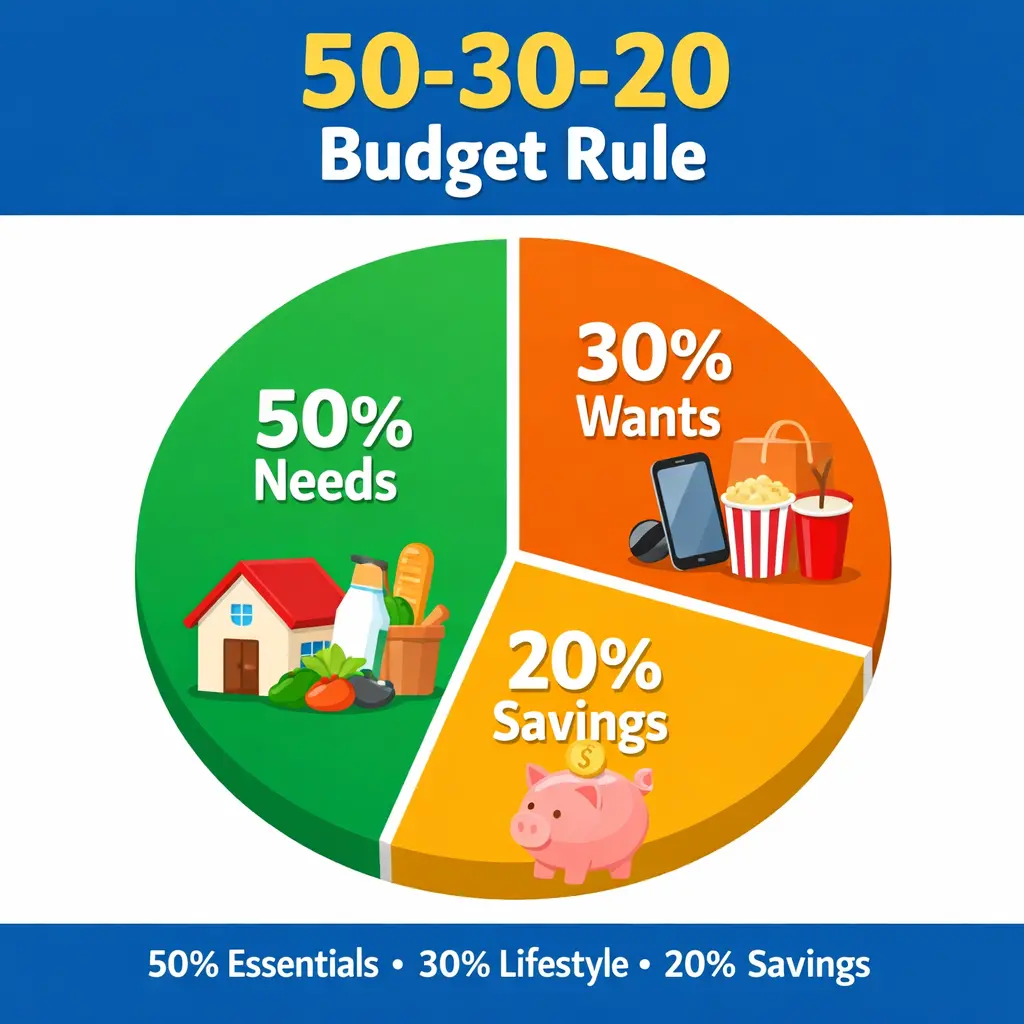

Basic Needs vs Wants in Budgeting

It does not make sense to know something if you are not going to use it. I began to change the way I spend my money by using this one simple rule

- 50 percent → Needs

- 30 percent → Wants

- 20 percent → Savings

This is a globally recognized rule by Elizabeth Warren that helps people balance their lifestyle and savings without feeling restricted.

What changed for me? I did not stop spending on wants. I just became aware. For example, I reduced food ordering instead of eliminating it. Also, I delayed unnecessary purchases and tracked where money was going. This is where needs vs wants budgeting actually works.

Needs vs Wants Budget: What Actually Works

One shift made the biggest difference. Earlier, I used to think: “I will save whatever is left.” Now, I follow: “I will spend whatever is left after saving.” This changed my behavior completely. Because now:

- Needs are covered first

- Savings are protected

- Wants are controlled

Final Thought

Understanding what I need vs what I want is not about the money I have. It is about being aware of my spending. I still buy things that I really enjoy. I do not think it is a good idea to never let myself have anything I want. Now I know exactly why I am spending my money.

That one change makes a big difference. It gives me control over my money. Because in the end, problems with money do not happen all of a sudden. Money problems are built up slowly through the choices I make every day, choices that I never really think about.

Disclaimer: This article is written for general educational purposes and is based on practical understanding and real-life examples. It does not provide professional financial advice, and readers should consult a qualified expert before making any financial decisions.

Have any thoughts?

Share your reaction or leave a quick response — we’d love to hear what you think!

-

0

0

-

0

0

-

0

0

-

0

0

-

0

0

-

0

0